Author: Shakil Shah, CFA

Improvements in collateral quality, regulatory oversight and more robust structures have encouraged some institutional investors to re-enter the European securitisation market, says Shakil Shah.

The housing crisis in the US and its link to mortgage-backed securities (MBS), is widely considered one of the causes of the Global Financial Crisis (GFC). However, while the crisis originated in US MBS, it quickly spread across the securitised spectrum, damaging investor confidence, and significantly reducing the volume of issuance.

Over a decade on, the US market has recovered and is at the forefront of innovation in the securitised space, but Europe, and to a lesser extent the UK remain scarred from the 2008/09 experience, even though the majority of pre-crisis structures that were not directly in the eye of the storm paid in full.

Despite the reluctance of the continental European market to embrace the new crop of securitisations, improvements in collateral quality, regulatory oversight and more robust structures have encouraged some institutional investors to re-enter the market and issuance has consequently picked up. In an ultra-low interest rate world, the yield on offer from securitisations is proving attractive and has led to a strong increase in issuance in collateralised loan obligations (CLOs) in particular.

Figure One: Issuance in the European markets since 2011 across the main sub-sectors

Source: JP Morgan Markets; Citigroup; Bloomberg

Although levels of issuance remain well below pre-GFC levels (in Europe less than a third compared to the height of the market in 2006/07), the securitised market today has returned to become an important financing tool for capital markets with a breadth of subsectors offering varied return and risk profiles. Underpinning the market, in contrast to earlier issues, is the quality of underlying collateral pools. The problems in the US housing market triggered a retrospective look into the failings that caused one of the worst recessions in recent history. The result was a vast improvement in lending standard on both sides of the Atlantic, not just in mortgage markets but also other loan markets such as auto financing and credit cards.

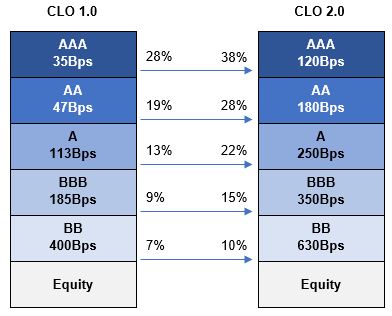

The shortcomings of credit rating agencies were also examined, and more stringent rating criteria has meant that structural protections have been widely improved to address rating standards. Among the many aspects of structure, credit enhancement is often the most quoted and simplest to reference when comparing pre-to post-crisis bonds. Taking the CLO market in Europe as an example, the entire credit spectrum has moved up a notch making a pre-crisis AAA bond equivalent to an AA bond today.

Figure Two – Evolution of credit enhancement and average spreads from pre-crisis (CLO 1.0) to post-crisis (CLO 2.0)

Source: Moodys Analytics; Payden

In addition, innovation, predominantly in the US, has presented investors with enhanced opportunities as well as relieving the burden faced by the taxpayer at times of crisis. For example, the US credit risk transfer (CRT) market has developed and aims to privatise an element of the collateral held by the large US mortgage agencies, so called Government Sponsored Entities. Introduced in 2013, this market has evolved steadily buoyed by a newly robust US housing market and growing investor confidence.

Beyond residential mortgages, annual new issuance volumes in the commercial sector have doubled since 2012. The challenges of the Covid crisis over the previous two years notwithstanding, commercial property types are varied in range and size, allowing those focused on the sector to extract value even at times of stress. The commercial real estate (CRE) CLO sector is a particular area of growth. Much like a corporate CLO, a CRE CLO is a managed pool of commercial real-estate loans with varied property types and geographic locations.

Accessing Value

The pandemic adversely impacted the office and retail real estate markets, but the diversity of the asset class has allowed investors to rotate investment opportunities to securities with a higher concentration to flats and warehouses which have benefited from the online delivery boom. Although this market is skewed towards the US, Europe is starting to realise the value of these types of structures, and importantly the need to diversify funding away from traditional sources such as banks.

Following the challenges of the last few years, central bank and fiscal largesse has supported families and markets in trying times. Technological advancements and science are propelling society forward, and as 2022 kicks off, Western economies are contending with rising energy and labour prices, and the related uncertainty around potential central bank tightening in developed Western markets. In this context, the securitised market has the potential to remain attractive to investors due to its return potential versus more traditional fixed income asset classes, its largely floating rate base, and diversified investor base. The former is starkest in the European market where, modest tightening notwithstanding, very low interest rates are likely to persist for some time, and so competitive real returns in markets such as CLOs, residential MBS, commercial MBS and some areas of consumer and commercial asset backed securities should hold the sector in good stead.

This positive view should not preclude investors from assessing the underlying risks and undertaking extensive examination of the range of structures within current securitisations. But for those with the experience and determination to add value, the securitised market is likely to be increasingly attractive and so witness continued growth. Prudence is important and the risk of rising interest rates in major markets should not be discounted even if the underlying reference rate on many securitised bonds resets higher as rates move up not to mention the impact rising living costs could have on consumer demand. While the probability of a steep and prolonged period of interest rate hikes cannot be ruled out (thus leading to volatility in credit markets), the more likely scenario is a gradual rise in rates to more ‘normal’ levels. In this context, the securitised market has the potential to remain an outperformer, bolstering the sector’s value in a balanced investment approach.

Shakil Shah, CFA, is responsible for credit and strategy for European structured products at Payden & Rygel.